.png)

Just a year or so ago, Generative AI was still seen as a novelty in banking circles impressive, but maybe not immediately practical. Fast forward to today, and it’s become a strategic priority. Since OpenAI’s breakout in late 2022, the boardroom conversation has shifted. It’s no longer “Will Gen AI change banking?” — it's now “How fast can we implement it at scale?”

And the numbers back it up. According to EY, Gen AI could unlock anywhere between $200 to $400 billion in annual value for the global banking sector that’s nearly 9–15% of total operating profits.

In short, it’s a game-changer not just for efficiency, but for competitiveness. Banks that act now are setting themselves up to lead the next era of finance. Those who delay? They may find themselves scrambling to catch up. For decision-makers, the real challenge is no longer “if” it’s choosing which use cases to bet on first and figuring out how to make Gen AI a core part of the bank’s digital transformation journey.

Beyond Digitization: What Gen AI Brings to the Table

Generative AI promises to add not just efficiency, but a new layer of intelligence across banking operations. At its core, GenAI excels at processing unstructured data the kind that traditional systems have long struggled with. This includes everything from customer emails, loan documents, KYC forms, voice conversations, and handwritten PDFs, to regulatory filings and call center transcripts.

While conventional AI is restricted to structured datasets and narrow functions, GenAI’s large language models (LLMs) are trained on vast corpora of information, enabling them to learn semantic patterns, understand context, and generate language, insights, or decisions in real time.

This unlocks a fundamentally different kind of capability. Instead of hard-coded rules and linear decision trees, GenAI adapts, reasons, and communicates.

For example, a GenAI-powered assistant can distinguish whether a customer asking about a “statement” is referring to a monthly balance, a loan disclosure, or a suspicious transaction based on tone, past queries, and intent. It can then escalate, resolve, or act autonomously based on internal policy. In treasury or corporate banking, GenAI can instantly pull key financial metrics from dense reports and draft investment memos for decision-makers, dramatically reducing turnaround time.

In short, we’re entering an era of cognition-driven transformation. GenAI is becoming a thinking partner, not just a digital assistant able to observe, interpret, and contribute meaningfully to decision-making. For banks, the question is no longer whether to adopt it, but how to embed it deeply into every workflow that demands intelligence, speed, and judgment.

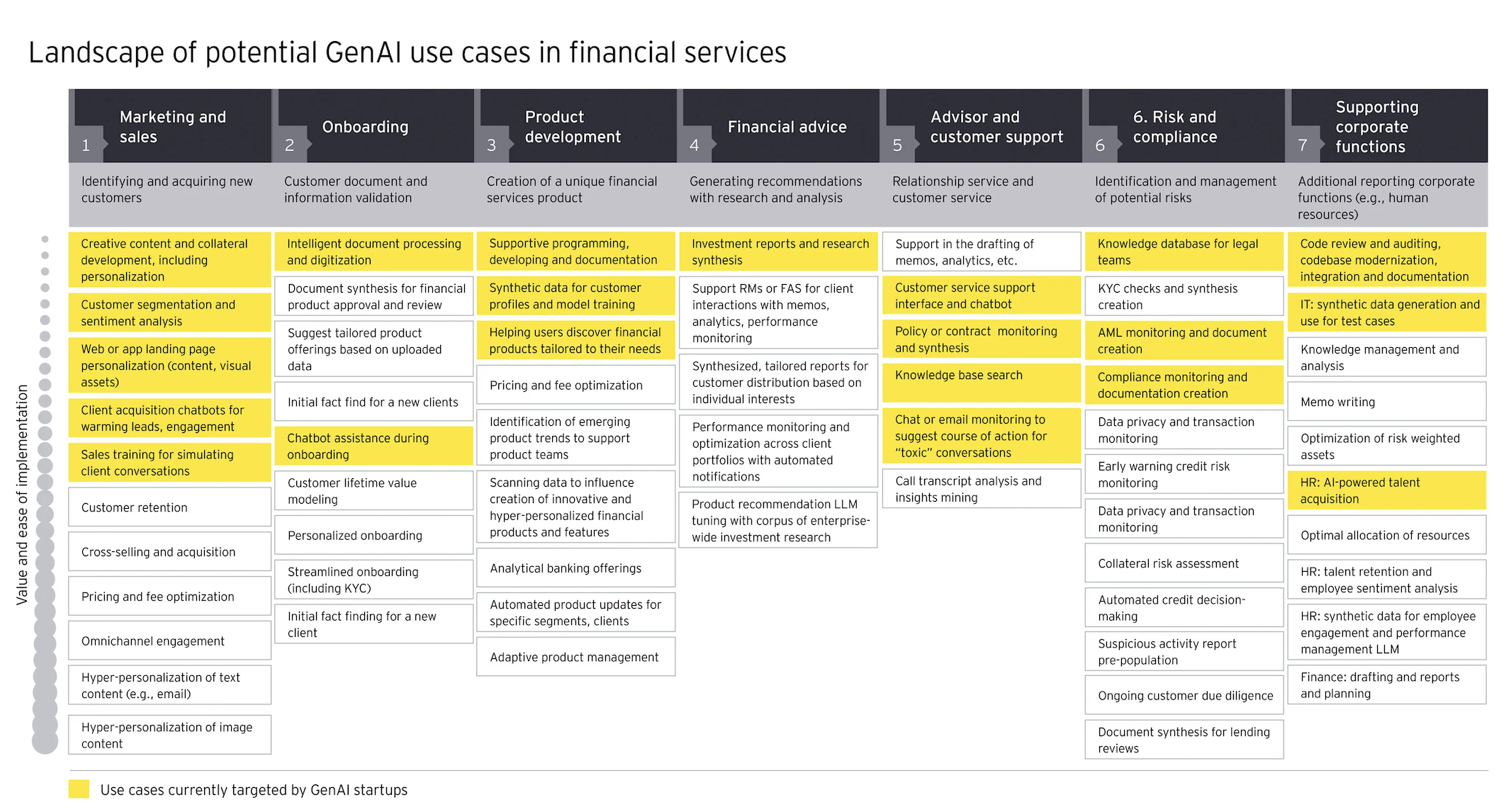

Where GenAI Delivers ROI

Banks are already unlocking tangible value from GenAI across three major domains. These aren’t theoretical use cases they’re proven deployments delivering measurable ROI:

- Retail Banking: The retail segment focuses on customer-facing innovations. Gen AI is elevating how banks engage millions of individual customers through personalized financial coaching, smart chatbots in mobile apps, conversational interfaces in ATMs, and even AI-driven personal finance management tools.

Smart assistants and personalization engines. For example, Bank of America’s “Erica” virtual assistant has handled 800 million client queries for 42 million users, delivering personalized guidance and even jokes to customers. Capital One’s Eno assistant, for instance, cut call-center volume by ~25% and raised customer satisfaction ~15%, saving ~$5 million per year.

In short, AI chatbots and financial coaches can answer routine questions instantly, nudge people on saving or fraud alerts, and dramatically reduce manual support load.

- Commercial & Transaction Banking: Banks are piloting GenAI tools to automate underwriting, draft loan memos and credit write-ups: AI reads customer filings, extracts key data, and generates draft reports for credit officers. This accelerates deal approval: one institution saw underwriting speed multiply by nearly 7× (making small-business credit decisions in minutes instead of hours).

Corporate clients benefit too banks use AI to forecast cash flow and trade finance needs by analyzing invoices, market data and more. Early adopters report thousands of hours saved annually on loan docs and compliance checks, as relationship managers can focus on exceptions rather than data gathering. Even in technology teams, GenAI boosts productivity – one bank saw ~40% faster coding and development when developers used AI assistants.

- Investment Banking and Markets: In the capital markets, investment banking, and wealth management arena, generative AI is becoming a force multiplier for knowledge work. Research and advisory functions leverage AI to condense massive amounts of information into digestible analysis. Investment banks are experimenting with AI to draft sections of investor pitch decks and deal prospectuses, based on data inputs and past deal knowledge – effectively auto-generating a starting proposal that bankers can refine.

In markets divisions, traders and portfolio managers use AI assistants to parse live market news and perform rapid scenario analysis (e.g. “Explain how today’s Federal Reserve comments might affect our bond portfolio”). This helps firms react faster in fast-moving markets. A high-profile example in wealth management is Morgan Stanley’s deployment of a generative AI assistant “AskResearchGPT” to its financial advisors: it indexes tens of thousands of research reports and internal documents so advisors can instantly query information and even get a summary of a client’s last meeting.

This significantly cuts down research time and ensures advice is up-to-date and well-informed. Moreover, investment firms are using gen AI to test trading strategies on simulated data, generate code for quantitative models, and automate parts of compliance.

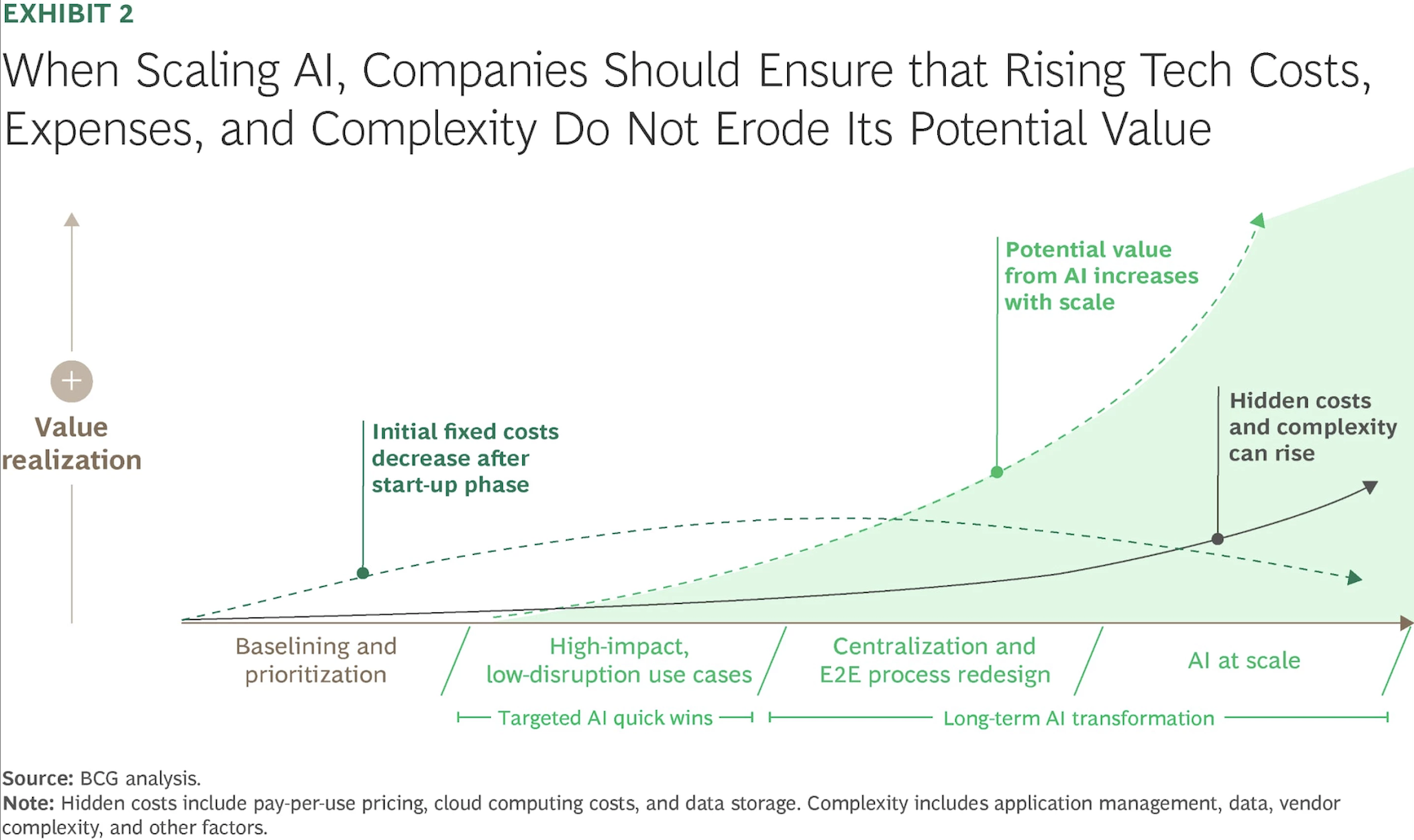

The Value Curve of GenAI: Scaling vs. Complexity

Generative AI promises exponential value but realizing that value is neither immediate nor linear. A recent BCG analysis illustrates a critical truth about AI transformation: while the potential value of AI increases with scale, so too do the hidden costs and operational complexities if not carefully managed.

What the Curve Tells Us:

- Start Small, Scale Smart

In the early phase baselining and prioritization banks incur fixed costs related to infrastructure, data integration, and talent onboarding. These upfront investments are necessary, but they begin to yield returns as the organization identifies high-impact, low-disruption use cases like AI assistants for customer support or automated report generation.

- Unlock Quick Wins Without Major Disruption

These “targeted AI quick wins” offer tangible ROI while building confidence across the organization. Examples include: automating KYC extraction, using GenAI for call center summarization, or automating underwriting processes.

- The Inflection Point: Redesign vs. Runaway Complexity

As organizations centralize efforts and redesign end-to-end (E2E) processes, the real gains begin to show. Here, value realization accelerates—but only if governance, data infrastructure, and change management keep pace. Without it, costs related to vendor sprawl, application management, cloud usage, and security risks can surge neutralizing benefits.

- AI at Scale: The Payoff and the Pitfalls

In the final stage, where AI becomes a scaled capability across the bank, the potential is transformative intelligent workflows, predictive operations, and hyper-personalized experiences. But reaching this point requires strong foundations and tight orchestration. Otherwise, hidden costs (e.g., uncontrolled cloud usage, duplicate tooling, integration debt) can balloon.

Implementing Generative AI: The C-Suite Playbook

Adopting generative AI in banking isn’t just about technology, it’s about reshaping people, processes, and infrastructure.

.jpg)

1. Align AI with Strategy and Governance

- C-Suite Ownership: Over 60% of banking leaders now place Gen AI on the CEO’s agenda. Top-down alignment ensures AI delivers business value, not just tech novelty.

- Centralized Oversight: Establish AI Centers of Excellence to drive governance, reduce duplication, and scale successful use cases.

- Outcome-Focused Investment: Link AI initiatives to measurable business goals (e.g., improved onboarding time, fraud reduction).

- Responsible AI: Update risk frameworks to manage hallucinations, bias, and model opacity. Deploy guardrails, validation workflows, and human-in-the-loop systems.

2. Upgrade Data and Cloud Infrastructure

- Unify & Enrich Data: Break down data silos, focus on unstructured inputs (PDFs, calls, emails), and implement robust tagging and governance.

- Cloud-Ready Architecture: With only 31% of banks moving half their workloads to the cloud, scalable Gen AI demands faster cloud adoption. Use secure, financial-grade platforms.

- Modern Tools: Embrace vector databases, ML Ops pipelines, and sandboxing environments to deploy and iterate Gen AI models at scale.

3. Build Talent and Drive Change

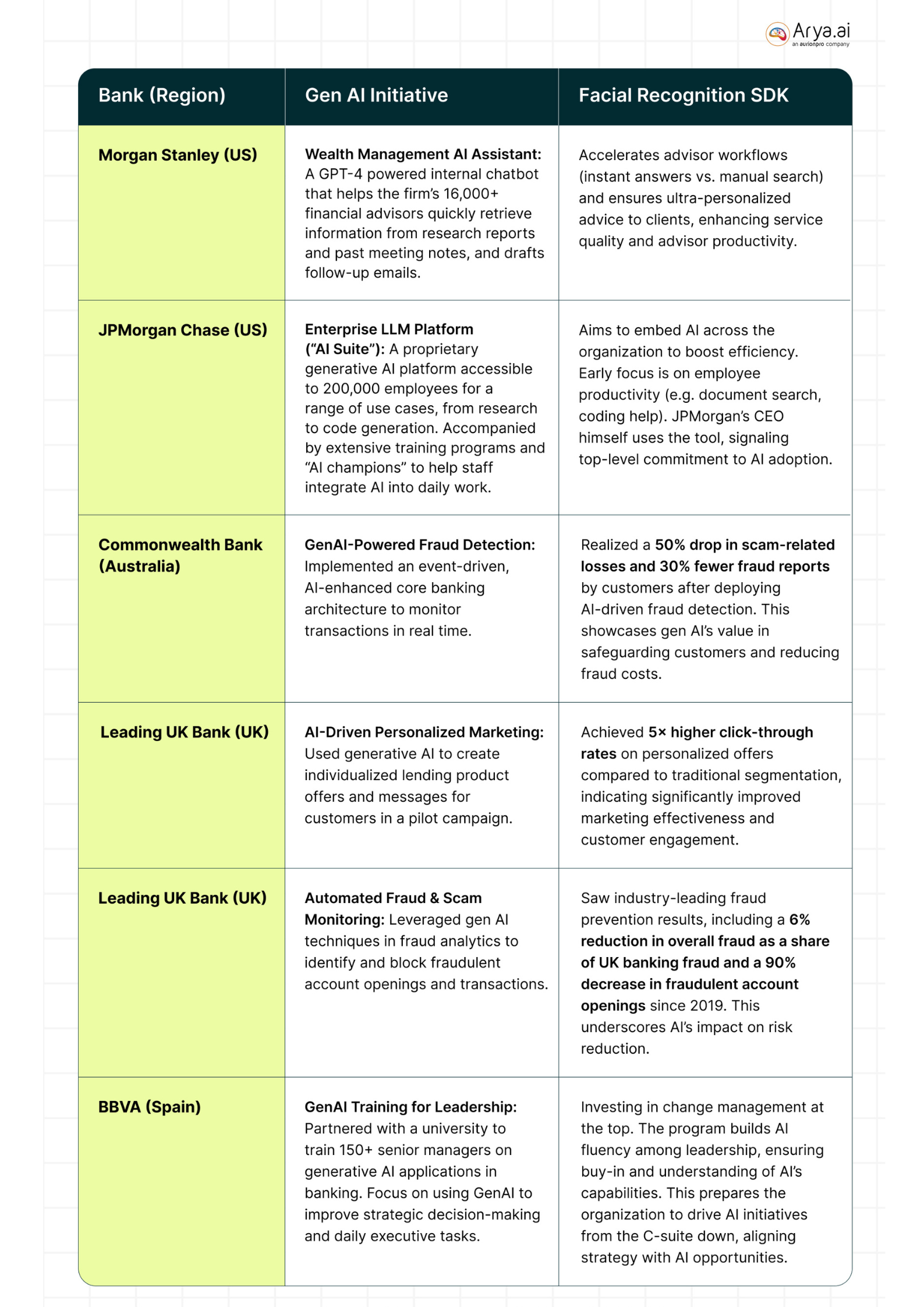

- Leadership Buy-In: Train executives to understand Gen AI’s potential and risks. BBVA and JPMorgan already do this.

- Workforce Upskilling: Introduce roles like prompt engineers and AI stewards. Launch “AI academies” to raise organization-wide fluency.

- Show Value Early: Use lighthouse projects to demonstrate ROI and gain buy-in. Reassign impacted roles instead of cutting them.

- Embed AI in Workflows: Redesign daily tasks to integrate AI naturally. Use ambassadors and incentives to boost adoption.

4. Start Small, Scale Fast

- Prioritize Quick Wins: Launch in high-impact areas like customer support or IT co-pilots. Use lessons to scale cross-functionally.

- Enterprise Scaffolding: Build common infrastructure and reusable tools that enable consistent, rapid AI deployment.

- Link Applications: Combine capabilities (e.g., chatbot + call summary + auto-email) to unlock end-to-end automation.

5. Build vs. Buy vs. Partner

- Smart Resourcing: Build in-house for core IP, buy commoditized tools, and partner for speed or niche expertise.

- Integrated Stack: Ensure AI tools fit legacy environments. Industry platforms like Microsoft’s Financial Services Cloud help with compliance.

- Fill Gaps with Ecosystem: Tap into AI startups, consultancies, and universities to scale fast while developing internal capabilities.

Read More: Build vs. Buy: Navigating the AI Agent Dilemma in BFSI

Wrapping it up

Generative AI marks more than just another step in digital transformation it’s a profound shift in how banks operate, serve, and grow.

The early results are clear: better customer experiences, faster decision-making, and meaningful gains in efficiency. But capturing this value at scale requires more than isolated pilots. It calls for clear vision, strong foundations, and a culture ready to evolve.

Banks that move with purpose aligning GenAI to strategy, governance, and day-to-day operations will not only lead the next chapter of financial services but help shape it.

This is a moment of opportunity. And the banks that choose to lead with intelligence, responsibility, and speed will define what’s next.

Share this post

.png)

.svg)