.png)

Underwriting teams have automated most of the operational grunt work. In the last decade, automation has expanded into data ingestion from credit bureaus and KYC sources. Simple projections and scorecards are also visible in dashboards. Rule-based systems can route workflows and send applications for approval/rejection.

This type of automation reduced the turnaround time and headcount, but it never truly answered the questions that matter:

- Is this revenue real or artificial?

- Is this cash flow stable or staged?

- Is this borrower over-leveraged in ways we can’t see yet?

These are interpretive questions. They require context across time, entities, and instruments. These are the areas where credit underwriting teams still spend hours.

Here, simple rule-based automation will not work. The team needs a solution that can weave context across transactions. It should answer what the transactions mean, not which category they belong to.

Why Bank and Financial Statements?

Bank and financial statements reliably decipher financial behavior. Invoices, pay stubs, and P&Ls can be polished. On the other hand, bank and financial statements are much harder to distort. If underwriting teams would like to learn how the money moved, the credits vs debits ratio, the money movement sequence, reversals & overdrafts, and so on, these statements have the answer!

They show what actually happened:

- How money moved

- With whom

- In what sequence

- With which corrections, reversals, and overdrafts

That’s why the future of credit risk isn’t just “more data sources.” It's interpretation of statements as a single source of behavioral truth.

The Interpretation Gap

Most lenders today sit in an awkward middle ground. They have invested in automation that can ingest statements and parse transactions. But when the credit committee needs to understand whether a borrower's revenue is sustainable or whether cash-flow patterns signal distress, someone still opens a spreadsheet and starts reading line by line.

This is the interpretation gap. Automation answers "what happened." Interpretation answers "what does it mean, and should we care?"

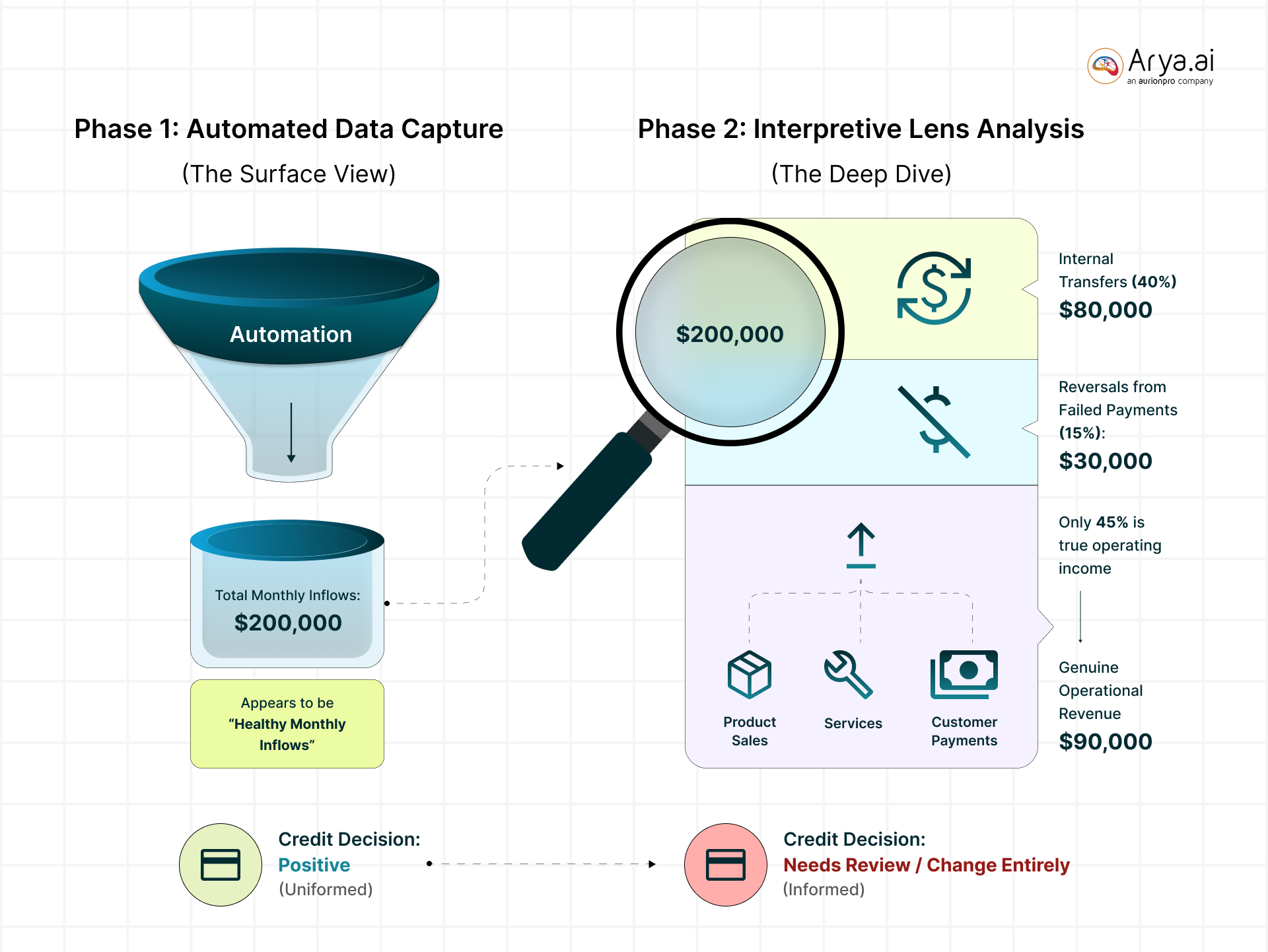

Consider a simple example. A mid-sized business shows healthy monthly inflows of $200K. Automation captures this accurately. But an interpretive lens reveals that 40% of those inflows are internal transfers between the borrower's own accounts, another 15% are reversals from failed payments, and the genuine operational revenue is closer to $90K. The credit decision changes entirely.

Today, catching this requires an experienced analyst spending hours cross-referencing transaction descriptions, counterparties, and timing patterns across months of statements. This is more of a comprehension problem than a data one.

What Interpretation Actually Looks Like

Interpretation in credit underwriting refers to a fundamentally different capability: the ability to read financial behavior as a seasoned analyst would, but at scale and with consistency.

This means several things in practice.

First, it means isolating true revenue from noise. Not every credit to a bank account is income. Transfers, refunds, loan disbursements, and round-tripping all inflate the top line if you are simply summing inflows. An interpretation layer separates operational revenue from non-business credits, giving underwriters a clean picture of earning capacity.

Second, it means detecting patterns over time. A single month's statement is a snapshot. Three to six months of statements, read together, reveal trends — recurring income streams that signal stability, seasonal dips that explain temporary shortfalls, or a gradual deterioration in cash reserves that a point-in-time check would miss entirely.

Third, it means surfacing anomalies that matter. Not every unusual transaction is a red flag. But circular fund movements before a loan application, sudden spikes in high-value payments to previously unseen counterparties, or a pattern of overdrafts that gets papered over by end-of-month deposits — these are signals that an experienced underwriter would catch, and that a rule-based system would likely miss because they do not fit neatly into predefined categories.

The goal is not to replace the underwriter's judgment. It is to ensure that by the time a file reaches the credit committee, the interpretive work has already been done — accurately, consistently, and in seconds rather than hours.

Automation Needs Intelligence

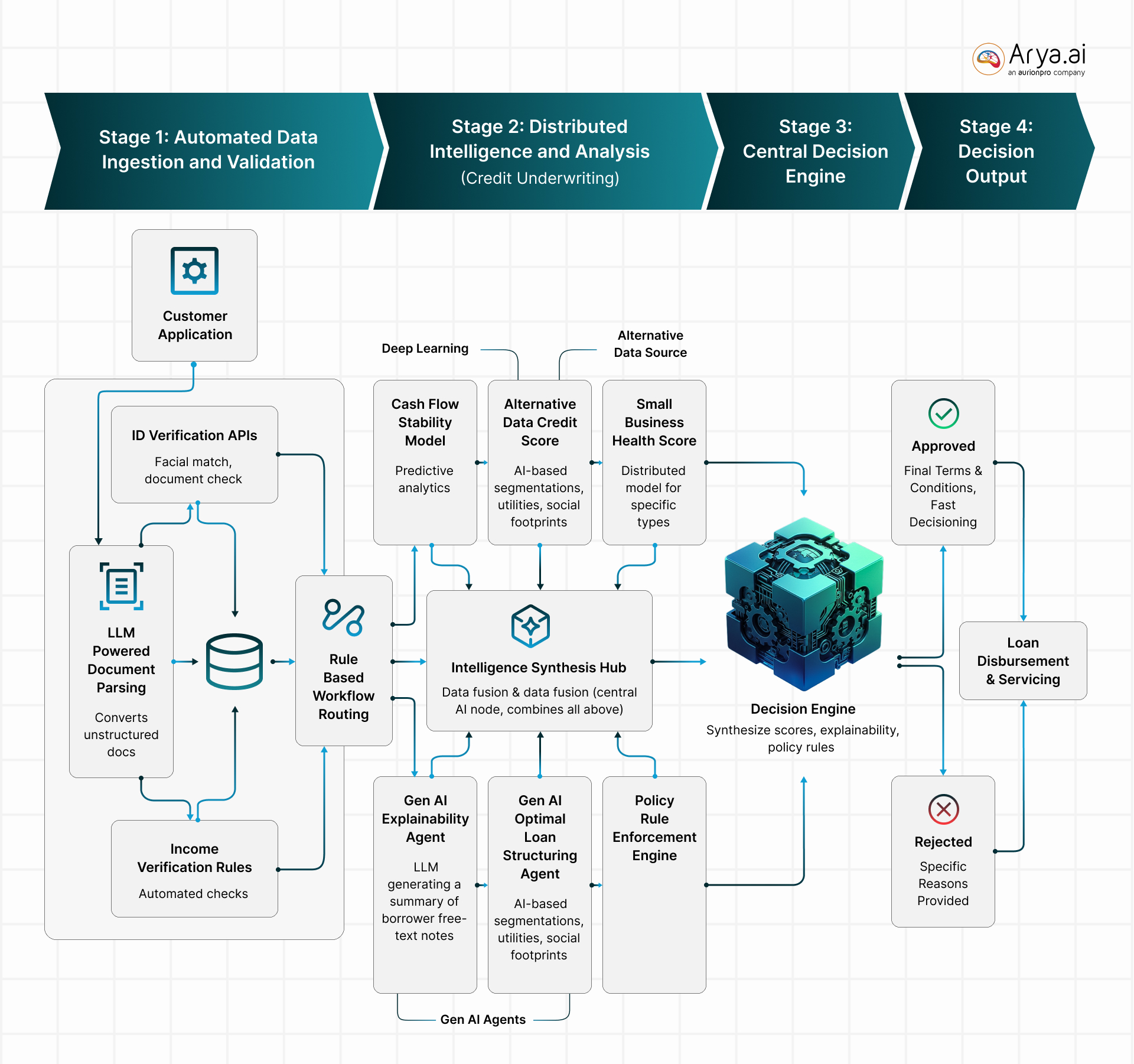

Rule-based automation will remain key in lending operations. Data ingestion, workflow routing, policy rule enforcement, and so on optimize the throughput. However, areas such as credit underwriting require intelligence. These are the areas that consume a significant chunk of lending teams’ time.

The industry must move toward automation rooted in intelligence so that decision pipelines can be augmented. You cannot get this with rule-based automation. This is not a theoretical distinction. It is already playing out.

Leading fintechs and banks globally are coupling such rule-based systems with deep learning models and Gen AI. Inevitably, the leaders who get this right stand to not only make faster decisions but are rich in insights and auditable. If you get this right, faster decision-making will automatically follow.

Where Do You Start?

For lending leaders evaluating their next investment in underwriting infrastructure, the question is no longer "how do we automate more?" It is "how do we interpret better?"

That starts with statement intelligence (both bank and financial statements): the ability to extract, classify, and contextualize transaction-level data into decision-ready insights. It means moving from raw PDFs to structured understanding: true revenue, recurring income patterns, repayment capacity forecasts, anomaly detection, and cash-flow narratives that a credit committee can act on immediately.

Solutions like Arya.ai's Cred AI are emerging to address exactly this gap. Cred AI can turn statements into a unified intelligence layer that plugs into existing loan origination systems and delivers interpretive depth at automation speed.

The future of credit risk is not about processing more data faster. It is about understanding what the data is actually telling you. The lenders who build for interpretation today will own the credit decisions of tomorrow.

Share this post

.png)

.svg)