.png)

Ask any senior banker what keeps them up at night, and you'll rarely hear "AI strategy" as the first answer. You'll hear about onboarding backlogs that stretch to six weeks. About the credit ops team running overtime to clear the month-end queue. About the third regulator letter this quarter, asking for evidence of the decision-making process. About the cost-to-income ratio that refuses to budge, no matter how many transformation programs get launched.

This is the gap that Agentic Process Automation (APA) is quietly closing, and it is the reason the conversation has shifted, almost overnight, from "should we pilot AI?" to "which processes do we hand over to agents first?"

If you've been watching this space from a distance and wondering whether it's another rebrand of RPA, this one is worth a closer look.

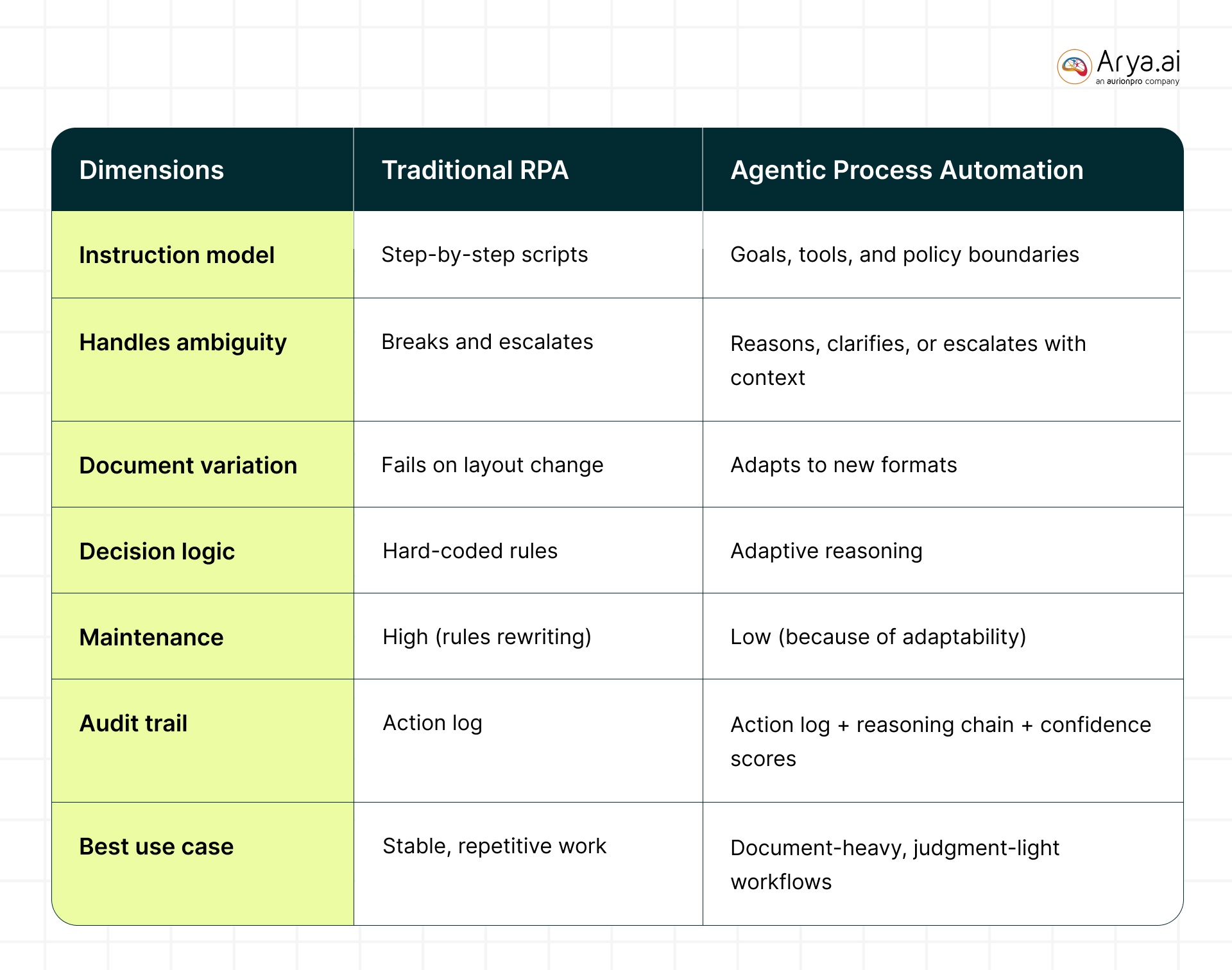

RPA promised the bots. Agents are what showed up.

For the better part of a decade, banks invested heavily in Robotic Process Automation. The pitch was elegant: take the swivel-chair work out of the back office, let bots click through legacy screens, free up humans for higher-value tasks. And in fairness, RPA delivered real value, until it didn't.

The problem was brittleness. RPA bots are deterministic. They follow scripts. The moment a field moves, a document arrives in an unexpected format, or a customer answers a question in a way the flow didn't anticipate, the bot breaks, and a human is paged. The result, for most banks, was a sprawl of hundreds of bots maintained by a small army of developers, each one a single point of failure dressed up as automation.

The difference is worth seeing side by side:

Agentic Process Automation is built on a fundamentally different premise. Instead of scripting every step, you give an AI agent a goal, a set of tools, and a policy boundary, and it figures out the path. It reads the document even if the layout has changed. It asks a clarifying question if the customer's answer is ambiguous. It escalates when it's not confident. It writes its own audit log as it goes.

What an agent does inside a bank: four workflows worth examining

Abstraction is the enemy of buy-in. Let's look at four processes where APA is already showing measurable results.

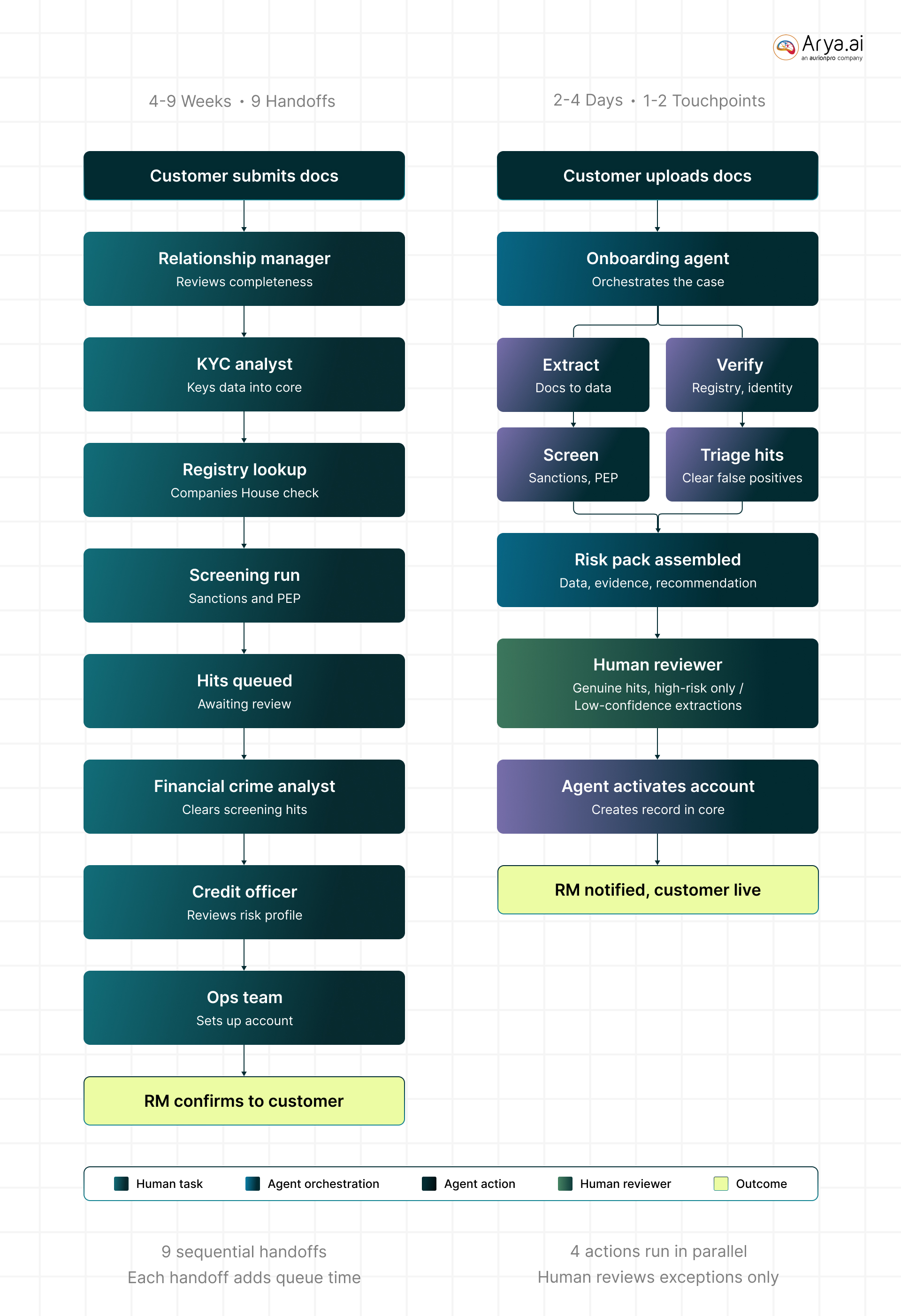

Workflow 1: Business onboarding

Commercial onboarding is the most painful process in most banks. A typical SME case touches five or six teams over four to six weeks. Here is what the traditional flow looks like versus the agentic onboarding version.

The reviewer is still in the loop, but they're reviewing twenty cases a day instead of completing four. That is the unlock.

Workflow 2: Transaction monitoring alert triage

Every large bank generates tens of thousands of AML alerts a week. Industry false-positive rates sit between 95% and 99%. The result: large investigation teams spending most of their time clearing noise.

An agentic alert triage workflow looks like this:

- An alert arrives from the transaction monitoring system with a rule reference and the underlying transactions.

- Triage agent pulls the customer's profile, recent transaction history, peer-group benchmarks, and any prior SARs or open cases.

- Agent reasons over the pattern: Is this transaction consistent with the customer's stated business? Does the counterparty appear in any negative news? Is the structuring pattern explained by a known event like payroll or a tax deadline?

- The agent produces one of three outputs:

- Auto-close with full reasoning recorded (low-risk, high-confidence false positive)

- Escalate to an L1 analyst with a pre-populated investigation pack

- Escalate to L2 / SAR consideration with elevated context

- Every action is logged with the model's reasoning chain, the data sources consulted, and a confidence score.

The compliance officer's quality assurance team samples a percentage of auto-closes for review. The agent learns from disagreements.

The point here is not that the agent replaces the investigator. The point is that the investigator's day shifts from triaging noise to investigating signal.

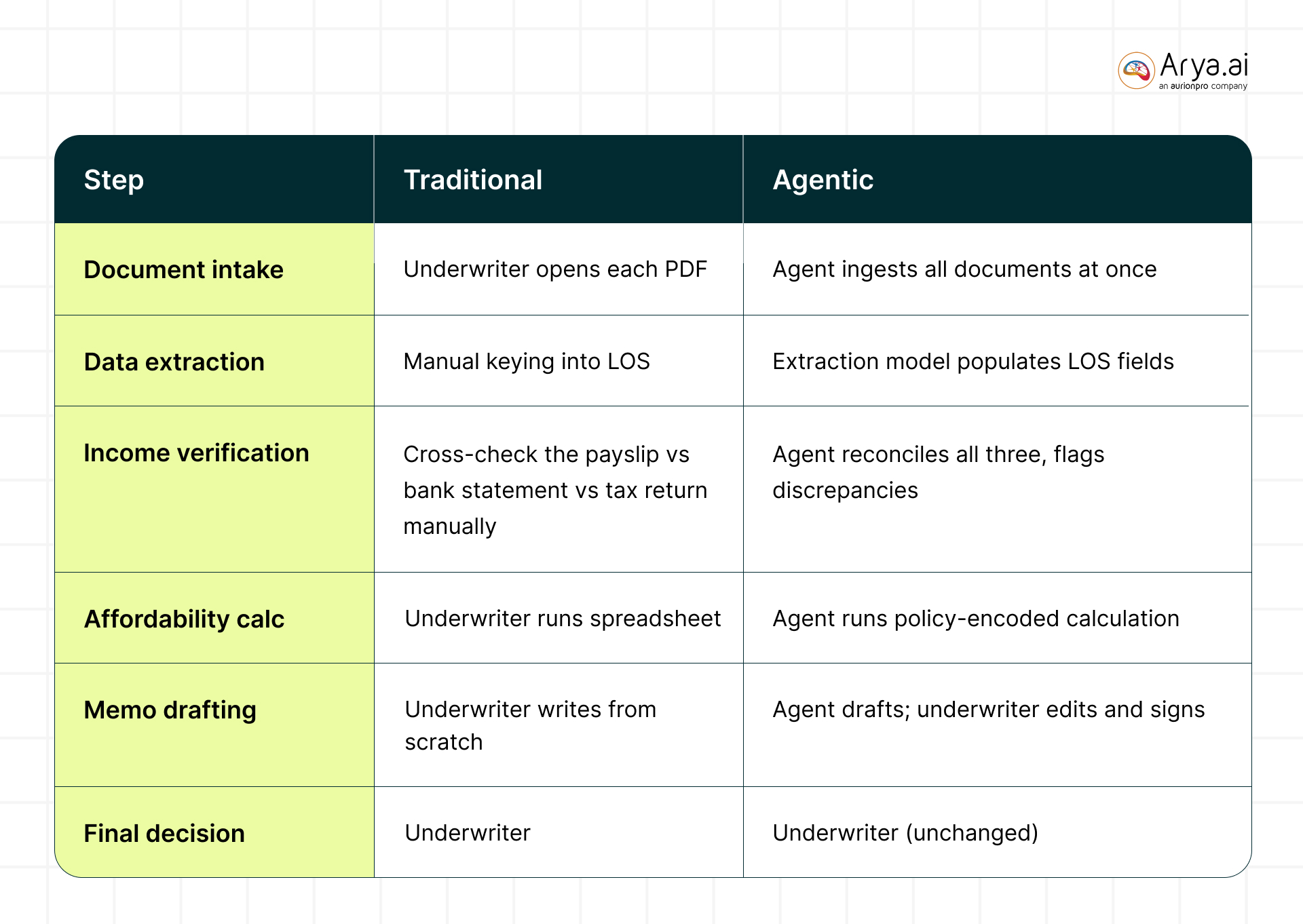

Workflow 3: Mortgage document review

A mortgage application generates a stack of documents: payslips, bank statements, tax returns, employer letters, proof of deposit, and property valuation. A human underwriter currently reads all of them, keys in the relevant fields, runs affordability calculations, and writes a credit memo.

The agentic version produces a case for an AI-powered mortgage document review that cannot be overlooked:

The final credit decision stays with the human. What changes is that humans spend their time on judgment calls rather than assembly work.

Workflow 4: Dispute and chargeback handling

Card disputes are high-volume, document-heavy, and policy-driven, almost a textbook APA fit.

The four shifts that make this real

Four things have changed in the last eighteen months that make this conversation different from previous AI hype cycles.

Reasoning quality. The current crop of foundation models can hold a complex policy in working memory, apply it to a specific case, explain its reasoning, and flag its own uncertainty. That last part matters more than people realize. A model that says "I am 73% confident this is a match; here is what would change my mind" is a system you can govern. A model that simply spits out an answer is not.

Tool use. Agents can now reliably call APIs, query databases, fetch documents, and chain those actions together. The integration work that used to take months can increasingly be configured in days. A single agent can talk to your core banking system, your CRM, Companies House, your sanctions provider, and your case management tool, and orchestrate across all of them.

Memory and context. Agents can hold the state of a long-running case, the back-and-forth with the customer, the documents received, and the checks completed, without losing the thread. This is what makes them usable for processes that span weeks, not just for one-off queries.

Auditability. Modern agentic frameworks are being built with regulatory readiness as a first-class concern. Every action the agent takes is logged. Every decision has a traceable chain of reasoning. Every escalation has a recorded trigger. For a CRO or a head of compliance, this is the bit that turns a curiosity into a serious procurement conversation.

Where to start (and where not to)

The instinct in most banks is to start with the biggest, hairiest process, usually because that's where the cost is. This is almost always the wrong move.

The processes where APA pays back fastest tend to share three characteristics: they are high-volume (so savings compound), document-heavy (because that is where current models genuinely shine), and have clear policy boundaries (so the agent's behavior can be tightly scoped and tested).

Here is a rough map of where to start and where to wait:

The pattern is straightforward: get the foundations right on processes where the agent is doing assembly work and the human makes the consequential decision. Expand the perimeter as your governance muscle develops.

The governance question that actually matters

Every banker reading this is asking the same question: how do I explain this to the regulator?

The honest answer is that the regulatory frameworks are evolving, but the underlying expectations are not new. Model risk management principles, embedded in SR 11-7, the EU AI Act, the PRA's supervisory statements, GDPR Article 22, and the NIST AI Risk Management Framework, are the same principles you already apply to credit models and AML scoring engines. Documented purpose. Validated performance. Ongoing monitoring. Human oversight of consequential decisions. Clear lineage from input to output.

What agentic systems require, that traditional models did not, is a more sophisticated approach to runtime governance. It's not enough to validate the model once and put it in production. You need:

- Continuous evaluation of the agent's behavior against a golden set of cases that grows over time.

- Automated guardrails that prevent the agent from taking actions outside its defined remit, hard limits, not soft preferences.

- A clear human override mechanism for any decision that crosses a defined threshold (transaction value, customer segment, risk band).

- Explainability on demand: Every agent decision should be reconstructable on request, with the inputs, the reasoning, the data sources consulted, and the policy applied.

- A kill switch. If the agent starts drifting, you need to be able to stop it instantly, without taking down the rest of the operation.

The better APA platforms now ship with these capabilities built in. The weaker ones don't. Procurement teams that treat this as just another software purchase tend to learn that distinction the hard way.

The strategic question for the next twelve months

Here is the uncomfortable truth that most bank executives already sense but few have articulated. The competitive gap between banks that adopt APA seriously and banks that wait is going to open up faster than previous technology cycles, because the leverage compounds.

A bank that automates onboarding doesn't just reduce costs. It reduces time-to-revenue for new customers. It improves the customer experience at the most fragile moment of the relationship. It frees up its best analysts to work on the cases that actually require judgment. It generates a richer dataset on which to train the next generation of agents. Each of those advantages reinforces the others.

The banks that move first on this will not look more efficient than their peers. They will look like different institutions altogether.

The right question is not "what does agentic automation cost?" The right question is "What does it cost us to still be running these processes the old way in two years?"

That is a conversation worth having on the next executive committee agenda.

Share this post

.png)

.svg)